Whether you own a wholesale or retail business, you have inventory. In fact, almost any business has inventory to some extent. Inventory is the component stock on hand to manufacture the goods you sell or it’s the goods themselves. Inventory control includes the methods used to manage the inventory you have in stock. This includes everything from how many items you have on the shelf to how much they cost and the amount of time it takes to replenish your stock.

Inventory is the cornerstone of any wholesale or retail business. In this guide, we will cover the benefits of using an automated inventory control system and discuss the challenges with inventory control. Additionally, we’ll describe the more common methods of inventory control and tracking.

Inventory management is the process of ordering and storing raw materials and finished products. It is the science of gauging the market, forecasting sales, and ordering. Inventory management is high-level inventory oversight. It forecasts the dance between having too much or too little inventory.

Inventory control is a subset of the inventory management process with a focus on operations. Inventory control includes day to day activities such as receiving raw materials, products, or other inventory, checking for any discrepancies, storing and transporting inventory to and from customers as well as within the warehouse. Inventory control also includes managing returns.

| Inventory Management | Inventory Control |

| Inventory management is a holistic process of planning, forecasting, and executing a series of inventory-related tasks for a company. | Inventory control consists of targeted activities such as sending orders, receiving stock, storing, and handling other day-to-day processes. |

| Inventory management has a much broader scope. | Inventory control has a limited, well-defined scope. |

| Inventory management uses powerful tools and software to understand and forecast current market trends to help businesses plan an effective inventory strategy. | Uses first-in-first-out (FIFO) and last-in-first-out (LIFO) techniques to chart and execute an inventory control plan. |

| Effective management includes efficiency analysis. | Inventory control defaults to business strategies set by management. |

| The goal of inventory management is to meet market trends and improve the bottom line. | The goal of inventory control is to effectively manage the inventory in stock at any given time. |

An inventory control system is a technical solution used to manage all facets of inventory management. The purpose of an inventory control system is to maintain the least amount of inventory in stock to improve cash flow by lowering holding costs. A robust system tracks goods through the supply chain including purchasing, shipping, receiving, warehousing, and returns. It should show you what inventory you have, where it is, and when you need to reorder.

The best systems operate in real-time to provide an accurate picture of what’s in stock, where it’s located, and when it’s time to reorder. Inventory control systems give you a bird’s eye view of your best-performing inventory as well as any bottlenecks or other problems with moving inventory. Computerized systems reduce human error.

How much you spend on inventory impacts every part of your business. Better inventory control equates to higher profit margins.

An inventory control system has many moving parts. This is contrary to antiquated paper and pen solutions. Manual inventory systems relied on honesty and integrity – where throwing a freebie into the order may have appeared to be goodwill but in fact cut into company profits. Manual inventory control requires headcount and is more susceptible to human error.

User-friendly, powerful inventory control systems like Cin7 give you all the advantages of a dedicated solution.

In its simplest form, inventory includes all of the items that a business uses for production or sale to an end user – it’s the gateway for businesses to earn a profit. The end user can be a business or individual. In the case of a manufacturer or wholesaler, the end user is another business. These business types operate business-to-business (B2B). We here at Cin7 also refer to them as major retailers like Target and Walmart. Conversely, a product seller operates business-to-consumer (B2C). Either way, these business structures have inventory; thus, need to manage that inventory.

Inventory can be defined as a necessary evil. It’s a dance between having enough to meet the needs of your customers but having nothing sitting on the shelves collecting dust. Inventory makes money for your business when it sells and it costs money when it’s doing nothing more than collecting dust.

In accounting terms, inventory is considered an asset. When inventory turns over (is sold), it represents one of the primary sources of revenue generation. Having just the right amount of inventory is the key to generating earnings for your business and your shareholders.

There are three primary types of inventory: raw materials, work-in-progress, and finished goods. These are the array of component goods used in production or finished goods for sale as part of the company’s normal course of business.

Raw materials are used to produce finished goods. Work-in-progress is as the name suggests – inventory that is somewhere between raw materials and finished goods. Finished goods are ultimately what the consumer will purchase, whether that consumer is a business or end consumer.

There are a number of other items considered inventory that are not necessarily categorized as one of the three primary types. For example, goods that are used in the production of products such as cleaning supplies, machines, and personal protective equipment (PPE). While these are not considered raw materials, and not part of the finished product, they are inventory and a necessary part of business.

Here we’ll explain the 12 different inventory types as well as the kinds of businesses that have each.

Raw materials are items used to manufacture a finished product or the individual component parts that collectively make up the finished product. Raw materials can be produced in-house, or they can be secured from a vendor. As an example, a chocolate manufacturer needs cocoa beans (raw material) to make a finished product. The manufacturer can grow the beans or source them from a supplier.

If you are outsourcing raw materials, timely arrival from suppliers is necessary to ensure smooth manufacturing operations. However, that is delicately balanced with quality. Just as you cannot build a house on a poor foundation, you cannot create a quality finished product with inferior raw materials.

Purchasing raw materials is a direct expense for the business.

The work-in-progress inventory refers to the components in use to make the finished product; however, the product is not entirely ready for sale. In simple terms, WIP is the partially completed product. For example, WIP inventory might be a table that still needs legs attached.

WIP inventory cannot be sold until it’s finished. Nonetheless, it occupies space in your facility; thus, costs money. Too much WIP inventory is bad for business – WIP inventory can raise storage costs without securing revenue.

Some business models require upfront payment or a deposit prior to manufacturing a product. In those instances, the WIP inventory has already generated revenue. This is common for custom-made orders. For example, beds are often manufactured once sold. In this instance, it can take longer for the customer to receive the final product, but it costs less for the business, and those savings can be passed to the consumer.

These are the goods that have been completed by the manufacturing process or purchased in a completed form. Finished goods have yet to be sold to the customer – whether that is a business or consumer. Like raw materials, finished goods can be entirely manufactured by the business or outsourced from a supplier.

Finished goods is the stock inventory available for customers to purchase. Most businesses prioritize finished goods.

Also known as decoupling stock, this process refers to separating inventory within the manufacturing process to mitigate one stage of the manufacturing process from slowing down another stage. Manufacturers set aside extra raw materials or WIP for some or all stages in the production line. In the event of low stock, delays in the supply chain, or a breakdown in one stage, production doesn’t stop further down the line. The finished product can still be manufactured.

The MRO goods are components needed in the manufacturing process but are not part of the final product. Examples include:

MRO goods are either consumed or discarded within the production process.

Another example of MRO goods are laptops and a WiFi connection. Unless you are in the business of selling laptops, your computer doesn’t directly bring in revenue. But if you’re a content marketer, your computer is used for writing, video editing, and designing – it is the machine that generates revenue.

It’s crucially important to maintain MRO inventory to avoid detrimental impacts to the quality of your final products. Mismanagement of MRO can also increase the risk of spoilage during the production process leading to losses.

Packaging is an integral part of the fulfillment process. As products are ready to sell, they need to be protected, and packaging protects them. Damage in transit can negatively impact the customer experience, leading to order returns.

According to Packaging Digest, 11% of all units that arrive at a distribution center are damaged. While often it may seem like a logistical problem, the root cause may be inefficient packing or packaging – yes these are different.

Packing involves protecting finished goods using wrapping such as bubble wrap or other wrapping. The goal of packing is to protect the product from damage.

Packaging is a box or outer wrapper designed to identify the brand. Packaging is brand identification. Another expectation associated with packaging is to identify the contents – whether with hazardous material labeling or fragile contents labeling. Appropriate labeling ensures the product will not be mishandled or opened in such a way as to destroy or damage the contents.

Safety stock is another term used to describe extra stock or inventory on hand to meet the needs of customers should there be a glitch in the supply chain. This form of inventory should be just enough to meet demand while waiting for supply to arrive. It’s a delicate balance between increased storage costs and dissatisfied customers.

Cycle stock is also referred to as working inventory. The amount of inventory that needs to be kept to meet the steady demand during a specific period. The amount of cycle stock is determined based on historical data and forecasts. Cycle stock is used to fulfill sales orders; thus, it needs to be regularly replenished to meet demand – it’s cycled.

Cycle stock is used to fulfill expected demand, whereas safety stock is used when cycle stock fails to meet that demand, or has yet to be replenished.

This inventory type applies to the service industry. Service inventory refers to the internal processes that allow an organization to rapidly respond to customer demands. For example, an airline makes money selling seats. If a seat remains empty, the flight loses money – it loses inventory. A set of internal processes, such as discounts and last minute deals affect whether that seat is sold.

Another example is a hotel. A hotel with 100 rooms has a monthly inventory of 300 stays (assuming a 30-day month). Restaurant inventory is the number of tables and bookings per hour over the time period the restaurant is open.

Other examples of service industry include advertising, healthcare, health clubs, and cloud computing. Any service business that sells “space” – that “space” is service inventory whether it is cloud space or a seat on a plane.

After products leave the warehouse, they become pipeline, or transit, inventory. This inventory type refers to what is moving between manufacturer, distributor, and retail outlet.

Pipeline inventory is somewhere in the shipping chain and has yet to reach its intended destination.

Obsolete or expired stock is excessive inventory. It is a liability for the company. It is not selling, so it costs the business money in terms of storage cost.

Inventory specifically intended to fulfill a surge in demand that is event-specific, like Christmas, is known as seasonal inventory. Seasonal inventory is also called anticipation inventory. Retailers must anticipate a spike in demand around holidays and forecast the products likely to draw shoppers. Under or over delivering will cost the business money in terms of lost opportunity, storage, or discounts.

In its simplest form, inventory control is the process of maintaining enough stock to meet customer demand without having a surplus. Inventory control avoids overstocking or understocking, or other issues that lead to losses including storage costs. It emphasizes reducing the number of slow-moving items while prioritizing those that sell quickly.

Proper inventory control improves cash flow and increases profit.

All types of inventory fall under the broad heading of inventory control – not just finished goods. Controlling stock is an effective way to mitigate inventory-related losses including:

Inventory control manages products from acquisition to final disposition – whether that is through sales or disposal.

The main objective of an inventory control system is to increase profits by identifying holes in the way you manage inventory.

Inventory control is an essential part of managing your business, just like purchasing, operations, quality control, feedback assessment, fulfillment, sales forecasting, and customer support. For most businesses, whether you’re a wholesaler, online retailer, or multichannel seller, tracking inventory efficiently is the only way to scale your business. Let’s look at some key objectives to having an inventory control system in place and what that will do for your business.

The primary purpose of an inventory control system is to ensure that all raw materials and finished goods are available either for production or for sale to end users. This includes all the inventory types necessary for your business to operate without a glitch.

Internal stock handling is a nightmare for many inventory managers because it is difficult to keep pace when all internal handling, recording, and tracking are done manually. An inventory control system is able to quickly show spikes in sales, promotions, and other factors to alert management to the necessary inventory response; thus, improving efficiency.

The different costs associated with inventory include labor costs, storage costs, ordering, and supply chain costs. All costs incurred by a business are either passed onto the consumer or can be responsible for the business failing. To prevent either, businesses can use an inventory control system to determine where money can be saved along the supply chain from acquisition to consumer.

Inventory directly or indirectly impacts almost everything that happens in your company. Employing an inventory control system will save money at multiple touchpoints. A streamlined inventory control system can increase your bottom line by helping to identify inefficiencies in shipping, handling, and storage costs.

Inventory has a way of disappearing – whether its intentional misappropriation (stealing) or product deterioration or obsolescence. Having a system in place is particularly effective at reducing losses. A computerized system with built-in checks and balances is much more difficult to manipulate than a manual inventory system. Additionally, managers can quickly determine which products are sitting on the shelves and discount or discontinue those items; thus, reducing waste.

Exceeding customer expectations is one way to stand out from the competition. A detailed inventory system can be key – knowing what you have, where you have it, or how long it will take to get it.

An essential advantage of having real-time inventory control reports is that they provide businesses with instantly actionable data. Additionally, real-time inventory management allows you to easily analyze trends and pinpoint where improvements are needed. Real-time reporting gives your business a competitive edge and improves sales by minimizing or eliminating stockouts.

Inventory control serves a vital function in estimating future sales volume or evaluating what items to put on sale racks. Forecasting is essential for retail businesses and a huge part of optimizing product sales. Using an inventory control system, business managers can review historical purchasing data to make assumptions based on performance.

Small businesses can benefit from automated inventory control at any stage, especially when the business begins to scale up in size. Integrating automated inventory control when the inventory is at a manageable level makes it that much more efficient as your company grows.

Implementing an integrated solution is the single most effective technique to ensure that every aspect of your company stays connected.

Knowing what to order, when, and how much requires a team effort. Using an automated solution improves communication because working as a team is integral to the inventory process.

The first line of communication is from production to sales and marketing. Marketing departments have a pulse on demand, whether through customer interaction or data, and production knows what’s in the works. Collaboration between these departments ensures minimum and maximum inventory limits are met without over producing or undersupplying.

The reorder point (ROP) is a specific level at which stock needs to be ordered so that you do not run out of inventory. Of course, a big part of determining the ROP is keeping a pulse on raw materials and work-in-progress goods in addition to finished goods. A robust inventory control system can be used to forecast the ROP for all the components used in production as well as finished goods.

There are a variety of inventory control methods available, and you can select the one that best meets your needs. Whatever approach you select, it’s critical that the strategies aid in determining minimum inventory needs as well as ROP.

Inventory control reduces costs and improves service. It also manages the working capital to maintain adequate and consistent cash flow. Effective inventory control is having the right product in the right place at the right time. Maintaining stock is essential in meeting customer expectations.

The primary objective of inventory control is to keep only the necessary units on hand without overspending or compromising customer satisfaction. Depending on your business, each comes with their unique idiosyncrasies, whether you’re an online retailer, wholesaler, or manage inventory throughout the supply chain.

Inventory control aims to increase profitability and efficiency by meeting customer needs without compromising profits. Inability to accurately count stock can lead to stockouts, unfulfilled orders, and disappoint customers.

The ordering experience should be fast and simple. Over a third of U.S. consumers consider purchasing from a different company following a poor experience.

To keep loyal and satisfied customers, you need to avoid or minimize customer complaints – proper inventory control helps you do just that. In addition, it helps you:

Consistently faulty suppliers and damaged inventory are the bane of an online retailer’s existence. Quality assurance and control helps track suppliers’ inventory. With the help of inventory control, you can quickly react to product recalls or other product defects. Proper quality assurance contributes to a positive company reputation.

Maintaining stable inventory levels is key to generating profits. Too much inventory leads to increased overhead expenses, and too little inventory prevents your business from keeping up with sales.

A robust inventory control system lets your business maintain a bird’s-eye view over your business. You become more resilient and able to avoid or mitigate out-of-stock scenarios.

Optimized inventory levels help deter:

Competition is fierce with online retailing. Customers can easily shop anywhere with just a few strokes of the keyboard. Inventory control is crucial to keeping customers on your site.

Inventory can be one of the largest expenses for your business, right behind payroll. Ensuring you store only what you need to meet your customers’ needs improves cash flow and profits. This is particularly important for wholesale businesses that often maintain large warehouse spaces.

An inventory control system identifies where the product is and how to find it in the warehouse. In addition to location, an effective system keeps track of quantity and ROPs.

An accurate system helps you organize your work within the warehouse. Essentially, knowing what you have, how much you have, and where it is in the warehouse increases picking efficiency.

In a large facility it is easy for things to become unorganized and for stock to get lost. Not only does this increase the incidence of deadstock, it makes it very difficult to manage the space efficiently.

An inventory control system is important for wholesalers who maintain larger amounts of inventory where hand-counting just doesn’t make sense. It minimizes understocking and overstocking.

Throughout the day, it is essential to keep track and monitor order fulfillment. A working inventory system manages day-to-day transactions in real-time ensuring orders are filled correctly and delivered to the right buyer. And, in the unfortunate event a product is returned, it is accounted for and properly disposed of, returned to the original manufacturer, or restocked for sale.

The supply chain includes the core activities required to turn raw materials into finished goods such as securing materials, manufacturing, and transportation to customers. Tracking the product as it moves through the supply chain is critical to avoid disruptions in distribution.

Inventory control along the supply chain is important to maintain a functioning supply chain.

Inventory turnover ratio is one of the key metrics for successful inventory management. It shows how much inventory is sold within a defined time period. Maintaining a balanced inventory turnover ratio is important to generate profit.

This ratio will let you know if you’re wasting money on stocking obsolete items or overstocking as well as if you have a break along the supply chain. A low inventory turnover ratio indicates too much of your inventory is sitting on the shelves. Whereas a high inventory turnover ratio means items are flying off the shelves. In other words, the demand is exceeding or just meeting supply. This can lead to deficiencies and lost profits as market demand changes.

An effective supply chain inventory management system ensures what comes in also goes out; thus maintaining cash flow through the business. The three core steps in inventory management include: purchasing inventory, storing inventory, and profiting from inventory.

When inventory is purchased, that money is tied up until that inventory sells – it’s essentially tied up in the promise (or hope) of a sale. Part of inventory control is data analysis that includes the lifecycle of inventory – from receiving to selling.

Inventory control can help businesses maintain a short cash conversion cycle (CCC). The shorter the CCC, the healthier the business is. The CCC is maintained when a company collects outstanding payments quickly, correctly forecasts inventory needs, or pays its bills slowly – running a short cash conversion cycle requires effective inventory forecasting.

The desired result of an efficient and lean supply chain is customer satisfaction. One way this is achieved is with same-day or 24-hour delivery schedules. Another is ensuring questions are answered and the correct products are sent.

An optimized supply chain results in fewer shipments and out-of-stock items and ensures delivery accuracy.

Handling a customer’s issue accurately and quickly goes a long way towards ensuring a positive brand image which leads to future business. One study showed that 45% of U.S. consumers will abandon an online purchase if their concerns are not addressed quickly.

Inventory control methods evaluate the accuracy of your inventory records against the actual physical inventory on hand. There are two methods for inventory assessment: periodic and perpetual.

The periodic inventory control method reconciles inventory on an occasional or periodic basis. The accounting period is determined based on the business needs. Merchandise is recorded in the purchase account. The inventory account and the cost of goods sold (COGS) account are updated at the end of the accounting period. The COGS shows the company’s gross margin. Gross margin is calculated by subtracting the COGS from revenue.

The inventory account is adjusted to match closing stock for the accounting period. The closing stock can be calculated using the first-in, first-out (FIFO) method or the last-in, first-out (LIFO) method.

The periodic inventory control method is cost effective and often preferred by small businesses. However, the challenge of periodic inventory tracking is the amount of time it takes to perform physical counts. Often normal business activities need to stop during the inspection period and significant human resources are required to perform the counts.

Additionally, there are no checks and balances between accounting periods. This makes it challenging to pinpoint when and where discrepancies may have occurred.

The perpetual inventory control method uses sophisticated equipment and software that tracks inventory in real-time. Updates are made automatically whenever a product is received or sold. Unlike periodic inventory control, perpetual inventory has a built-in checks and balances system because inventory is updated in real-time.

For businesses with multiple product lines and high sales volumes, a perpetual inventory system makes sense.

In the past, inventory control was managed using spreadsheets and manual audits. Accounting mistakes and inaccuracies lead to challenges in meeting fulfillment requests.

Now, automated and integrated systems have become the standard in all industries. Businesses can integrate financial data including accounts receivable and payable and customer history into one system. Future trends rely on cloud computing and real-time tracking.

Innovative, fully automated systems are the best way to stay ahead of competitors. As an example, just-in-time inventory tracks turnover ratios and alerts you of low inventory levels. Having this information enables you to quickly adjust to keep pace with demand.

Many automated systems offer shared software databases between businesses and suppliers. Benefits include efficient order fulfillment, customizable packaging, and improved customer service.

An inventory tracking system uses a dashboard, software, or program that tracks inventory in real-time. This type of inventory management adheres to the perpetual inventory method, offering instant accessibility to data.

Inventory tracking software generally integrates with a point-of-sale (POS) system to provide instant updates every time an item is scanned, sold, or shipped. It also provides valuable information for inventory forecasting.

Inventory software requires an upfront investment and a monthly payment for use. It is a comprehensive solution with numerous long-term benefits including:

Different systems are available for any size business, including periodic or perpetual inventory systems. However, a perpetual system is more suited to handle a large volume of stock or complex processes.

Whether you’re using a periodic or perpetual system, you’ll need a method to track inventory from the date of acquisition. Here are some common ways to achieve that:

Every business will face inventory-related challenges at some point, whether those are caused by internal or external factors. We won’t soon forget the global impact COVID had on the global supply chain.

Some events are beyond our control, while others are within our control. Either way, strategies can be developed to mitigate their effect. Let’s discuss some challenges you may encounter in the inventory control process, along with some practical strategies to resolve them.

On the surface, it might seem smart to hoard extra inventory to meet an unexpected surge in demand; however, this strategy often backfires leading to dead stock. Dead stock is unsellable inventory either because it has become obsolete, expired, or there simply isn’t any demand for the product. The shift from wired to wireless headphones is an example of loss of demand.

Overstocking increases holding costs and opportunity costs. Opportunity costs are those things missed for the sake of something else. In terms of inventory, overstocking on one product reduces capital available to purchase new products – it’s a loss of opportunity to make a profit from new products. On top of missed opportunities, there’s an increase in holding costs including storage, possible theft, or damage.

Dead stock is like quicksand – the more you stay in contact with it, the harder it is to get rid of. Here’s a few ideas to unload excessive inventory or dead stock.

Of course, we can’t always control external factors, like a global pandemic, but we can examine internal factors that lead to excessive or obsolete inventory. Often poor forecasting or overlooking trends in sales data contribute to overstocking.

Implementing regular stock auditing can identify inventory sales patterns and provide insights to when adjustment in stock levels are needed.

Stockouts occur when you do not have sufficient inventory to cater to the market demand.

Similar to having too much inventory, not having enough also affects cash flow. But more importantly, insufficient stock directly affects customer experience. Today’s shoppers expect same-day and next-day delivery. When they don’t, they’re quick to try other vendors or to write poor customer reviews.

(Image Credits)

While stockouts generally indicate you’re not utilizing your warehouse’s space to its maximum potential, there are several scenarios that may lead to stockouts. Some of the most common include current demand exceeding estimated demand, shortage in production, and disruption in the supply chain.

Safety stock can prevent or mitigate stockouts. Safety stock is a buffer of some additional inventory to safeguard your business from missing sales while waiting for inventory to arrive.

Safety stock formula

Safety Stock = [Maximum Lead Time x Maximum Daily Usage] – [Average Lead Time x Average Daily Usage]

To compute the amount of safety stock needed, you need to know the following:

Here’s an example. Let’s say on an average day you sell 50 units and the most you sell is 100 units. It takes five days to receive shipments from your supplier, and the maximum delay you’ve encountered is ten days.

Safety stock = [10 days x 100 units] – [5 days x 50 units]

This equals 750, meaning you should maintain a safety stock of 750 units to safeguard from a stockout.

Inventory shrinkage is when actual inventory is less than what is shown in your accounting ledger. There are several reasons for inventory shrinkage, such as:

Inventory shrinkage has a negative correlation with revenue, i.e., higher inventory shrinkage means less inventory on hand to sell. Having a strong inventory control system can help to resolve some of the causes or inventory shrinkage – especially in identifying theft, finding or minimizing miscounts and evaporations, and managing supplier theft. Supplier theft occurs when the stock received is less than the stock ordered.

Installing an inventory control system with barcode scanners can help eliminate stock counting errors caused by manual calculation, and effectively compute reorder points. Additionally, continual monitoring of inventory reduces theft, or, at the very least, identifies a problem early on.

One constant in retail is that demand fluctuates. Businesses need to adapt to changing customer demands – up and down the supply chain. Nokia was once the market leader in the mobile phone industry. However, they failed to adapt to the changing preferences of their customers and, as a result, lost their share in that market.

Adapting to changing demands can be taxing for businesses. Often this requires businesses to reconfigure manufacturing machines as well as acquire new raw materials. Businesses are constantly adjusting to fluctuations and adjustments caused by temporary surges in demand – especially demands for new fad products, like fidget spinners.

Inventory forecasting can help with demand fluctuations. To be effective, you’ll need accurate data that can help you spot trends and patterns. Without real-time visibility into your inventory, it can be difficult to know when to place or postpone a purchase order. In addition to accurate real-time data, efficient forecasting requires knowledge of lead time, present stock, and reordering point. It also helps to build strong relationships with your suppliers who might have vital information about trends in the marketplace.

Upgrading technology and investing in modern analytical tools will improve overall forecasting accuracy.

Did you know that only 63% of the time retail businesses actually get accurate inventory information? Misinformation can lead to errors in inventory management and make it challenging to reorder inventory on time, which can lead to shipping delays.

Dealing with inventory at multiple locations provides its own challenges. Compound those, when handling sensitive products such as pharmaceutical or food and beverage. In such industries, the role of inventory control goes beyond recording quantity. It also demands recording of information such as temperature and expiry information to meet safety regulations for end users.

Using a centralized information source – such as a robust inventory management system – will mitigate many of these challenges.

Centralization is not an issue for small businesses who maintain all their inventory in one place. The problem arises when a company expands and uses multiple warehouses to store its inventory. Using manual inventory records can make it difficult to share accurate real-time stock information.

A cloud-based inventory control system seamlessly monitors inventory in multiple locations and stores collected data in a centralized system.

Interestingly, 46% of small businesses still do not use an automated inventory tracking system.

Along with accurate data forecasting, clear communication amongst employees is also important. Lack of coordination among various departments increases operational inefficiencies. For example, when a stockout occurs, an inquiry is made to the purchase manager asking why an order wasn’t placed. In turn, the purchase manager responds that the warehouse manager indicated there was plenty of inventory in stock. Clearly, communication was not effectively coordinated through the pipeline. This is compounded when inventory is stored in multiple locations.

An automated system diminishes the likelihood of miscommunication between various departments.

In addition to communication and coordination inefficiencies, human error cannot be avoided in manually-driven systems.

Inventory tracking is an integral part of controlling inventory, and sets the foundation for inventory planning. Even as efficient as automated systems are, many businesses still utilize manual methods – such as printed lists – to keep track of their inventory. Manual tracking is time-consuming as well as prone to human error.

Manual counting, disconnected systems, and even outdated software can lead to data inaccuracy.

Using an automated stock tracking system is necessary to thrive in today’s retail world. Automated tracking systems use radio-frequency identification (RFID) or quick response (QR) codes to facilitate barcode scanning. Barcode scanning seamlessly counts inventory and stores that data in the cloud, providing accurate inventory information in real-time.

Irrespective of how robust your inventory control system is, a crucial human element is still required.

Hiring an inventory specialist who can manage all aspects of inventory including accurate data gathering is imperative for the success of your business. An inventory manager is responsible for:

Creating standardized guidelines and protocols to streamline workflows reduces instances of human error. To get the best results from your inventory control system, it is essential to invest adequately in modern technology and hire and nurture employees.

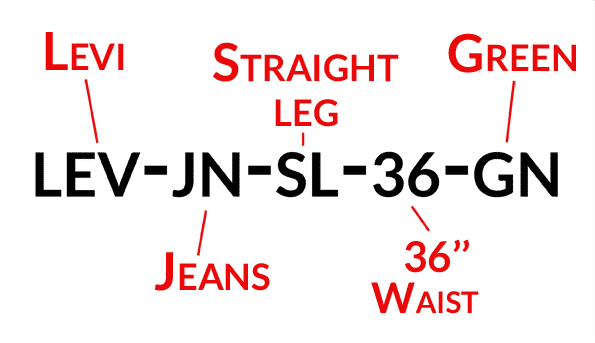

To develop a robust inventory control system, it’s necessary to accurately classify inventory as it sets the foundation for tracking and monitoring. Before diving into different inventory control techniques, it’s important to understand stock keeping units (SKUs) and product serialization.

SKUs and product serialization form the basis for internal classification. A SKU is an alphanumeric code representing the seller’s product. SKUs are used internally by the business to identify and classify its products.

There is no definite structure to creating SKUs; however, the SKU should provide information about the product, its components, and its size. Here is an example of SKU:

Utilizing a POS system can help create and manage SKUs. Access to SKU information is usually restricted to internal business staff. Your employees can efficiently look up product information by scanning the SKU number at a POS terminal. A POS system native to your inventory management software is ideal.

Product serialization keeps track of individual units of an inventory using serial numbers. Serialization helps with granular tracking and is commonplace with expensive luxury brands. Product serialization differs from SKUs in one primary way: Product serialization tracks an individual product through the life of the product. SKUs segregate product variants and are used in-house before the item is sold to the consumer.

Using iPhones as an example, SKUs identify the variants of each iPhone, their capacity, color, etc. The serial number tracks the device itself. When a consumer phones in for customer support, the serial number helps customer representatives retrieve specific information about that iPhone including manufacturing date, purchase date, etc. Product serialization can help determine whether the product is still under warranty.

Now that you’re familiar with SKU and product serialization, let’s get into the different inventory control techniques.

ABC classification is also referred to as the “Always Better Control” framework based on the Pareto principle. The Pareto principle states that 80% of the outcome is derived from 20% of total effort. The Pareto principle is also known as the 80/20 rule. The main principle of the 80/20 rule is that a significant part of the results are derived from a relatively small portion of the work. In business, this translates to focusing your efforts on the small portions that produce the most results. The ABC framework applies to inventory by classifying inventory into three major categories based on annual unit consumption.

Here is an example of a clothing retailer’s business using the ABC framework. To begin, let’s work through the step-by-step computation of ABC analysis. Step 1 – Compile data regarding the annual sales of each unit and associated manufacturing costs to determine annual usage value. Note: To calculate annual usage value, multiply annual units sold by cost per unit. The annual usage value for T-shirts is (5,000 x $20), or $100,000.

| Products | Annual Units Sold | Cost Per Unit | Annual Usage Value |

| T-shirt | 5,000 | $20 | $100,000 |

| Dress Shirt | 2,000 | $25 | $50,000 |

| Socks | 800 | $3 | $2,400 |

| Jeans | 700 | $30 | $21,000 |

| Trousers | 600 | $25 | $15,000 |

| Handkerchief | 500 | $5 | $2,500 |

| Night suit | 400 | $20 | $8,000 |

| Towel | 300 | $10 | $3,000 |

| Tracksuit | 900 | $25 | $22,500 |

Step 2 – Rearrange the products in descending order based on their annual usage value.

| Products | Annual Units Sold | Cost Per Unit | Annual Usage Value |

| Tshirt | 5,000 | $20 | $100,000 |

| Shirt | 2,000 | $25 | $50,000 |

| Tracksuit | 900 | $25 | $22,500 |

| Jeans | 700 | $30 | $21,000 |

| Trousers | 600 | $25 | $15,000 |

| Night suit | 400 | $20 | $8,000 |

| Towel | 300 | $10 | $3,000 |

| Handkerchief | 500 | $5 | $2,500 |

| Socks | 800 | $3 | $2,400 |

Step 3 – Calculate the sum of annual units sold and the annual usage value.

| Products | Annual Units Sold | Cost Per Unit | Annual Usage Value |

| Tshirt | 5,000 | $20 | $100,000 |

| Shirt | 2,000 | $25 | $50,000 |

| Tracksuit | 900 | $25 | $22,500 |

| Jeans | 700 | $30 | $21,000 |

| Trousers | 600 | $25 | $15,000 |

| Night suit | 400 | $20 | $8,000 |

| Towel | 300 | $10 | $3,000 |

| Handkerchief | 500 | $5 | $2,500 |

| Socks | 800 | $3 | $2,400 |

| Total | 11,200 | $224,400 |

Step 4 – Find the cumulative percentage of units sold and the cumulative percentage of annual usage value. Note: To calculate the cumulative percentage, divide the base value by the total value then multiply it by a hundred. The cumulative percentage for Tshirt is (5,000/11,200) x 100, or 44.64%.

| Product Category | Annual Units Sold | Cost Per Unit |

Annual Usage Value | % of Annual Units Sold | % of Annual Usage |

| Tshirt | 5,000 | $35 | $175,000 | 44.64% | 56.91% |

| Shirt | 2,000 | $30 | $60,000 | 17.86% | 19.51% |

| Tracksuit | 900 | $20 | $18,000 | 8.04% | 5.85% |

| Jeans | 700 | $30 | $21,000 | 6.25% | 6.83% |

| Trousers | 600 | $25 | $15,000 | 5.36% | 4.88% |

| Night suit | 400 | $20 | $8,000 | 3.57% | 2.60% |

| Towel | 300 | $10 | $3,000 | 2.68% | 0.98% |

| Handkerchief | 500 | $7 | $3,500 | 4.46% | 1.14% |

| Socks | 800 | $5 | $4,000 | 7.14% | 1.30% |

| Total | 11,200 | $307,500 |

Step 5 – Classify the data into A, B, and C categories based on the cumulative annual usage percentage. “A” category products should constitute 80% of the total annual usage; “B” should contribute 15%; and “C” should make up 5%. Every company will have a unique product mix, so the percentage values will vary slightly.

| Product Category | Annual Units Sold | Cost Per Unit | Annual Usage Value | % of Annual Units Sold | % of Annual Usage | Classification |

| Tshirt | 5,000 | $35 | $175,000 | 44.64% | 56.91% | 82.28% (A) |

| Shirt | 2,000 | $30 | $60,000 | 17.86% | 19.51% | |

| Tracksuit | 900 | $20 | $18,000 | 8.04% | 5.85% | |

| Jeans | 700 | $30 | $21,000 | 6.25% | 6.83% | 14.31% (B) |

| Trousers | 600 | $25 | $15,000 | 5.36% | 4.88% | |

| Night suit | 400 | $20 | $8,000 | 3.57% | 2.60% | |

| Towel | 300 | $10 | $3,000 | 2.68% | 0.98% | 3.41% (C) |

| Handkerchief | 500 | $7 | $3,500 | 4.46% | 1.14% | |

| Socks | 800 | $5 | $4,000 | 7.14% | 1.30% |

Now that the products are segregated into A, B, and C categories, here is what that looks like in terms of inventory control.

| Class | Degree of Control | Type of record | Frequency of review | Safety Stock | Management involvement |

| A | Tight | Accurate | Continuous | Small | Top-level |

| B | Moderate | Good | Occasionally | Medium | Middle-level |

| C | Loose | Simple | Less Frequent | Large | Bottom level |

These are the benefits of using ABC analysis:

Some drawbacks of ABC analysis include:

Unlike the ABC analysis, which classifies products based on their consumption value, VED analysis categorizes material based on their criticality for the business. VED is an acronym vital, essential, and desirable, each one a category. VED is used to classify items for a production schedule.

The VED analysis can be combined with the ABC method to classify products based on their necessity and consumption value.

| V | E | D | |

| A | AV (1) | AE (1) | AD (1) |

| B | BV (1) | BE (2) | BD (2) |

| C | CV (1) | CE (2) | CD (3) |

The ABC-VED matrix classifies products into three categories:

The table below summarizes how to work with each category:

| Category | Type of item | Degree of priority | Involvement of management |

| 1 | Vital and Costly | High | Top |

| 2 | Essential but less costly | Moderate | Middle |

| 3 | Desirable but not critical | Low | Bottom |

The FNSD analysis categorizes inventories into four groups based on descending order of usage. FNSD analysis emphasizes turnover: fast (F), normal (N), slow (S), or dead (D).

Slow turnover results from decreased demand for the product, overstocking, or is a sign of an inefficient stocking policy. It also reflects that a higher amount of capital is locked up in inventory that is not selling; thus, increasing carrying costs.

The VED, FNSD, and ABC analysis are inventory classification methods. Economic order quantity (EOQ) is a calculator used to determine ideal order size to meet demand without overspending. EOQ is calculated to minimize holding costs and excess inventory.

To calculate the EOQ, you need to know three variables:

After determining the variables, plug those into the formula to calculate EOQ. Let’s look at an example:

Jason owns a jeans shop. He sells 5,000 pairs of jeans a year. His wholesale cost for a single pair of jeans is $50, and his annual storage cost per pair is $10.

EOQ = √ 2(5000 x $50)/$10, which equates to 223.

According to the EOQ calculation, Jason needs to order 223 pairs of jeans to meet demand without overstocking.

The EOQ calculation considers the indirect relationship between ordering and holding costs – it finds the sweet spot between the two. This prevents ordering too much of a single item to achieve bulk pricing.

Although EOQ minimizes inventory costs and prevents stockouts, it works under the assumption that the demand remains constant – which is rare even in the best of times. Another limitation is that it can only be calculated for a single SKU at a time. So, depending on the number of products in your inventory, you’ll be doing a lot of math.

So far, we’ve covered how to classify inventory into different categories and determine the optimum ordering quantity, but what about stock replenishment? The reordering point formula is used to calculate the threshold, or point, at which a stock needs to be ordered to prevent stockout.

To calculate the reordering point, you’ll need to know the following variables:

The ROP is calculated using this formula:

Reorder point = (Lead Time x Average Daily Usage) + Safety Stock

Let’s use Jason’s jean store to show an example of how this works. He sells 5,000 units per year, so his average daily usage is 13 units (5,000 units / 365 days). His lead time is seven days, meaning it takes seven days to receive the shipments from his supplier. Jason maintains a two-week supply of safety stock, or 182 pairs of jeans (13 units x 14 days).

ROP = (7 x 13) + 182, which equates to 273 units.

So, when Jason’s inventory reaches 273 pairs of jeans, it’s time to reorder.

Robust inventory management software can be programmed to automatically place the order upon reaching ROP by enabling seamless reordering.

Other factors to consider with lead time and safety stock include:

Just-in-time (JIT) is an inventory control technique in which goods are purchased from the supplier only after receiving a customer order. It is also known as the zero inventory system. The primary objective of JIT is to minimize inventory holding cost and maximize the inventory turnover.

For JIT ordering to be successful, a robust supply chain structure is required to provide a smooth ordering and receiving process. Suppliers must be on-board with short notice and fast turn-around times.

There are some inherent benefits to JIT inventory management:

Although the JIT concept may sound ideal for minimizing holding costs and dead stock, it also has some drawbacks:

There are inherent benefits to investing in inventory control software early. Here are several:

Inventory and order management software is a set of business programs that track, manage, and organize product sales, material purchases, and other inventory activities. Businesses can employ systems based on barcodes or radio-frequency identification (RFID) which send real-time updates on products at every stage of the supply chain including acquisition, manufacturing, storage, and sale. Inventory management software automates many of the day-to-day processes related to inventory; thus freeing up valuable time for owners and managers to delight and inspire their customers.

Different systems are equipped with different capabilities, making it essential for operators to select an inventory management system that works with their business. Most software solutions are cloud-based and provide excellent scalability and versatility when businesses have multiple locations.

Cloud-based software like Cin7 eliminates the need for servers and IT staff. Cloud-based software is handled by Cin7; thus eliminating the need for a robust cybersecurity strategy.

Cloud-based software is typically available as a monthly subscription and should offer multiple integrations with other software businesses commonly use. This increases automation between programs.

Inventory management software improves the way you track products as they move through your company. It supports order management capabilities by replacing stock automatically at the right quantity. Automated inventory management software is essential for reducing human error and assisting your company to scale successfully. If you have any questions regarding inventory control, feel free to connect with us and get a Cin7 expert by your side.